Insurance cycle

The tendency to swing between profitable and unprofitable periods over time is commonly known as the underwriting or insurance cycle.

Definition

The underwriting cycle is the tendency of property and casualty insurance premiums, profits, and availability of coverage to rise and fall with some regularity over time. A cycle begins when insurers tighten their underwriting standards and sharply raise premiums after a period of severe underwriting losses or negative stocks to capital (e.g., investment losses). Stricter standards and higher premium rates lead to an increase in profits and accumulation of capital. The increase in underwriting capacity increases competition, which in turn drives premium rates down and relaxes underwriting standards, thereby causing underwriting losses and setting the stage for the cycle to begin again.[1] For example, Lloyd's Franchise Performance Director Rolf Tolle stated in 2007 that "mitigating the insurance cycle was the "biggest challenge" facing managing agents in the next few years".[2]

All industries experience cycles of growth and decline, 'boom and bust'. These cycles are particularly important in the insurance and re-insurance industry as they are especially unpredictable.

Lloyd's of London research in 2006 revealed, for the second year running, that Lloyd’s underwriters see managing the insurance cycle as the top challenge for the insurance industry, and nearly two-thirds believe that the industry at large is not doing enough to respond to the challenge.[3]

The Insurance Cycle affects all areas of insurance except life insurance, where there is enough data and a large base of similar risks (i.e. people) to accurately predict claims, and therefore minimise the risk that the cycle poses to business.

History

The insurance cycle is a phenomenon that has been understood since at least the 1920s. Since then it has been considered an insurance 'fact of life'. Most commentators believe that underwriting cycles are inevitable, primarily "because the uncertainty inherent in matching insurance prices to [future] losses creates an environment in which the motivations, ambitions, and fears of a complex cast of characters can play out."[4] Lloyd's counters that this has become "a self-fulfilling prophecy".[5]

More recently, insurers have attempted to model the cycle and base their policy pricing and risk exposure accordingly.

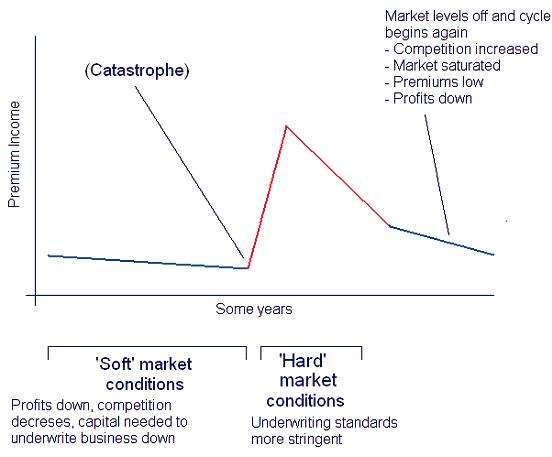

Description

For the sake of argument [6] let's start from a 'soft' period in the cycle, that is a period in which premiums are low, capital base is high and competition is high. Premiums continue to fall as naive insurers offer cover at unrealistic rates, and established businesses are forced to compete or risk losing business in the long term.

The next stage is precipitated by a catastrophe or similar significant loss, for example Hurricane Andrew or the attacks on the World Trade Center. The graph below shows the effect that these two events had on insurance premiums.

After a major claims burst, less stable companies are driven out of the market which decreases competition. In addition to this, large claims have left even larger companies with less capital. Therefore, premiums rise rapidly. The market hardens, and underwriters are less likely to take on risks.

In turn, this lack of competition and high rates looks suddenly very profitable, and more companies join the market whilst existing business begin to lower rates to compete. This causes a market saturation and Insurance Cycle begins again.

Dealing with the insurance cycle

While many underwriters believe that the cycle is out of their hands, Lloyd’s is trying to push for more proactive management of the ups and downs of the industry. In 2006 they published their ‘Seven Steps’ to managing the insurance cycle:

1. Don’t follow the herd. Insurers need to be prepared to walk away from markets when prices fall below a prudent, risk-based premium.

2. Invest in the latest risk management tools. Insurers must push for continuous improvement of these tools based on the latest science around issues such as climate change, and make full use of them to communicate their pricing and coverage decisions.

3. Don’t let surplus capital dictate your underwriting. An excess of capital available for underwriting can easily push an insurer to deploy the capital in unsustainable ways, rather than having that capital migrate to other uses such as hedge funds and equities, or returning it to shareholders.

4. Don’t be dazzled by higher investment returns. Don’t let higher investment returns replace disciplined underwriting as base rates creep up on both sides of the Atlantic. Notionally, splitting the business into insurance and asset management operations, and monitoring each separately, is one way to achieve this.

5. Don’t rely on "the big one" to push prices upwards. The spectacular insured loss should not be used as an excuse to raise prices in unrelated lines of business. Regulators, rating agencies, and analysts – not to mention insurance buyers – are increasingly resisting such behaviour.

6. Redeploy capital from lines where margins are unsustainable. There is little that individual insurers can do to alter overall supply-and-demand conditions. But insurers can set up internal monitoring systems to ensure that they scale back in lines in which margins have become unsustainable and migrate to other lines.

7. Get smarter with underwriter and manager incentives. Incentives for key staff should be structured to reward efficient deployment of capital, linking such rewards to target shareholder returns rather than volume growth.[7]

The Lloyd’s Managing Cycle report has several problems. It focuses on the industry as a whole being able to work together to reduce the effect of market fluctuations. However, this is somewhat unrealistic, as if underwriters do not write business in a soft market (i.e. at cheap prices for the customer), it will be hard to win this business back in a hard market due to loyalty issues.

Rolf Tolle asserts that "There is nothing complex about the cycle. It is about having the courage of your convictions to act with strength.".[8] Swiss Re argue that instead of ‘beating’ the cycle, insurers should learn to anticipate its fluctuations. "Cycle management is essentially proper timing. Monitoring the market, predicting market trends and accurately assessing prices play an important role".[9]

Swiss Re gave several examples of potential business strategies. One is to write risks at a roughly fixed rate. This is clearly not practical as it does not allow for the cyclical nature of the market. Another is to fail to react fast enough to changes in the market, which leaves a company even more exposed. The recommended strategy is one that relies on prediction of the business cycle and setting premiums based on models and experience.

The future of the insurance cycle

The unpredictable nature of the insurance industry makes it very unlikely that the cycle can be eliminated. For several years Lloyd's have been urging caution in soft periods and restraint in hard periods.

Notes

- ↑ "Analysis and Valuation Of Insurance Companies." Center For Excellence in Accounting and Security Analysis: Industry Study Two 2 (2003). http://www.columbia.edu/~dn75/Analysis%20and%20Valuation%20of%20Insurance%20Companies%20-%20Final.pdf (accessed 31 October 2012).

- ↑ Rolf Tolle, The cycle challenge - 12 July 2007, http://www.lloyds.com/News_Centre/Features_from_Lloyds/The_cycle_challenge.htm (accessed 21 August 2007)

- ↑ Lloyd's Annual Underwriter Survey, 2006 http://www.lloyds.com/News_Centre/360_risk_project/Managing_the_cycle.htm (accessed 21 August 2007)

- ↑ Fitzpatrick, Sean, Fear is the Key: A Behavioral Guide to Underwriting Cycles, 10 Conn. Ins. L.J. 255 (2004).

- ↑ Lloyd’s, Managing the Cycle – How the Market can Take Control http://www.lloyds.com/NR/rdonlyres/A27B9CEB-6F19-4364-BD0A-02AA92384544/0/360_ManagingtheCycle06_12_06.pdf (accessed 21 August 2007).

- ↑ The cycle has no start. It is a cycle. Obviously.

- ↑ Lloyd’s, Seven steps to managing the cycle, http://www.lloyds.com/News_Centre/Press_releases/Seven_steps_to_managing_the_cycle.htm (accessed 21 August)

- ↑ Todd, Cycle Challenge

- ↑ Swiss Re, The insurance cycle as an entrepreneurial challenge, http://media.swissre.com/documents/pub_the_insurance_cycle_as_an_entrepreneurial_challenge_en.pdf Accessed 21 August 2007