Racial inequality in the United States

Racial inequality in the United States refers to societal advantages and disparities that affect different races within the United States. These may be manifest in the distribution of wealth, power, and life opportunities afforded to people based on their race or ethnicity, both historic and modern. These can be seen as a result of historic oppression, inequality of inheritance, or overall prejudice, especially against minority groups.

Definitions

In social science, racial inequality is typically analyzed as "imbalances in the distribution of power, economic resources, and opportunities."[1] Racial inequalities have manifested in American society in ways ranging from racial disparities in wealth, poverty rates, housing patterns, educational opportunities, unemployment rates, and incarceration rates.[1][2][3][4][5][6] Some claim that current racial inequalities in the U.S. have their roots in over 300 years of cultural, economic, physical, legal, and political discrimination based on race.[7]

Political argument

Color blind racism

It is hypothesized by some scholars, such as Michelle Alexander, that in the post-Civil Rights era, the United States has now switched to a new form of racism known as color blind racism. Color-blind racism refers to "contemporary racial inequality as the outcome of nonracial dynamics."[3]

The types of practices that take place under color blind racism are "subtle, institutional, and apparently nonracial."[3] These practices are not racially overt in nature such as racism under slavery, segregation, and Jim Crow laws. Instead, color blind racism flourishes on the idea that race is no longer an issue in this country and that there are non-racial explanations for the state of inequality in the U.S. Eduardo Bonilla-Silva writes that there are 4 frames of color-blind racism that support this view:[3]

- Abstract liberalism – Abstract liberalism uses ideas associated with political liberalism. This frame is based in liberal ideas such as equal opportunity, individualism, and choice. It uses these ideas as a basis to explain inequality.[3]

- Naturalization – Naturalization explains racial inequality as a cause of natural occurrences. It claims that segregation is not the result of racial dynamics. Instead it is the result of the naturally occurring phenomena of individuals choosing likeness as their preference.[3]

- Cultural racism – Cultural racism explains racial inequality through culture. Under this frame, racial inequalities are described as the result of stereotypical behavior of minorities. Stereotypical behavior includes qualities such as laziness and teenage pregnancy.[3]

- Minimization of racism – Minimization of racism attempts to minimize the factor of race as a major influence in affecting the life chances of minorities. It writes off instances and situations that could be perceived as discrimination to be hypersensitivity to the topic of race.[3]

Manifestations of racial inequality

There are vast differences in wealth across racial groups in the United States. The wealth gap between white and African-American families nearly tripled from $85,000 in 1984 to $236,500 in 2009. There are many causes, including years of home ownership, household income, unemployment, and education, but inheritance might be the most important.[1]

Health disparities

Racial wealth gap

A study by the Brandeis University Institute on Assets and Social Policy which followed the same sets of families for 25 years found that there are vast differences in wealth across racial groups in the United States. The wealth gap between Caucasian and African-American families studied nearly tripled from $85,000 in 1984 to $236,500 in 2009. The study concluded that factors contributing to the inequality included years of home ownership (27%), household income (20%), education (5%), and familial financial support and/or inheritance (5%).[8]

Wealth can be defined as "the total value of things families own minus their debts." In contrast, income can be defined as, "earnings from work, interest and dividends, pensions, and transfer payments."[8] Wealth is an important factor in determining the quality of both individual and family life chances because it can be used as a tool to secure a desired quality of life or class status and enables individuals who possess it to pass their class status to their children. Family inheritance, which is passed down from generation to generation, helps with wealth accumulation.[9] Wealth can also serve as a safety net against fluctuations in income and poverty.[10]

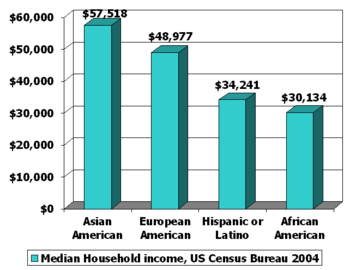

There is a large gap between the wealth of minority households and White households within the United States. The Pew Research Center's analysis of 2009 government data says the median wealth of white households is 20 times that of black households and 18 times that of Hispanic households.[11] In 2009 the typical black household had $5,677 in wealth, the typical Hispanic had $6,325, and the typical White household had $113,149.[11] Furthermore, 35% of African American and 31% of Hispanic households had zero or negative net worth in 2009 compared to 15% of White households.[11] While in 2005 median Asian household wealth was greater than White households at $168,103, by 2009 that changed when their net worth fell 54% to $78,066, partially due to the arrival of new Asian immigrants since 2004; not including newly arrived immigrants, Asian net wealth only dropped 31%.[11] As shown on "Eurweb - Electronic Urban Report"[12] According to the Federal Reserve Survey of Consumer Finances, of the 14 million black households, only 5% have more than $350,000 in net worth while nearly 30% of white families have more than this amount. Less than 1% of black families have over a million in net assets. while nearly 10% of white households, totaling over 8 million families have more than 1.3 million in net worth.

Lusardi states that African Americans and Hispanics are more likely to face means-tested programs that discourage asset possession due to higher poverty rates.[13] One-fourth of African Americans and Hispanics approach retirement with less than $1,000 net worth (without considering pensions and Social Security). Lower financial literacy is correlated with poor savings and adjustment behavior. Education is a strong predictor for wealth.[13] One-fourth of African Americans and Hispanics that have less than a high school education have no wealth, but even with increased education large differences in wealth remain.[13]

Conley believes that the cause of Black-White wealth inequality may be related to economic circumstances and poverty because the economic disadvantages of African Americans can be effective in harming efforts to accumulate wealth.[14] However, there is a five times greater chance of downward mobility from the top quartile to the bottom quartile for African Americans than there is for White Americans; correspondingly, African Americans rise to the top quartile from the bottom quartile at half the rate of White Americans. Bowles and Gintis conclude from this information that successful African Americans do not transfer the factors for their success as effectively as White Americans do.[15] Other factors to consider in the recent widening of the minority wealth gap are the mortgage crisis and credit crunch that began in 2007-2008. The Pew Research Center found that plummeting house values were the main cause of the wealth change from 2005 to 2009. Hispanics were hit the hardest by the housing market meltdown possibly because a disproportionate share of Hispanics live in California, Florida, Nevada, and Arizona, which are among the states with the steepest declines in housing values.[11] From 2005 to 2009 Hispanic homeowners' home equity declined by Half, from $99,983 to $49,145, with homeownership rate decreasing by 4% to 47%.[11]

History

Africans were first brought to the United States as slaves. While free African-Americans owned around $50 million by 1860, farm tenancy and sharecropping replaced slavery after the American Civil War because newly freed African American farmers did not own capital (land or supplies) and had to depend on the White Americans who rented the land and supplies out to them. At the same time, southern Blacks were trapped in debt and denied banking services while White citizens were given low interest loans to set up farms in the Midwest and Western United States. White homesteaders were able to go West and obtain unclaimed land through government grants, while the land grants and rights of African Americans were rarely enforced.[14]

After the Civil War the Freedman's Bank helped foster wealth accumulation for African Americans. However, it failed in 1874, partially because of suspicious high-risk loans to White banks and the Panic of 1873. This lowered the support African Americans had to open businesses and acquire wealth. In addition, after the bank failed, taking the assets of many African Americans with it, many African Americans did not trust banks. There was also the threat of lynching to any African American who achieved success.[14]

In addition, when Social Security was first created during the Great Depression, it exempted agricultural and domestic workers, which disproportionately affected African Americans and Hispanics. Consequently, the savings of retired or disabled African Americans was spent during old age instead of handed down and households had to support poor elderly family members. The Homeowner's Loan Corporation that helped homeowners during the Great Depression gave African American neighborhoods the lowest rating, ensuring that they defaulted at greater rates than White Americans. The Federal Housing Authority (FHA) and Veteran's Administration (VA) shut out African Americans by giving loans to suburbs instead of central cities after they were first founded.[14]

Inheritance and parental financial assistance

Bowman states that "in the United States, the most significant aspect of multigenerational wealth distribution comes in the forms of gifts and inheritances." However, the multigenerational absence of wealth and asset attainment for African Americans makes it almost impossible for them to make significant contributions of wealth to the next generation.[16] Data shows that financial inheritances could account for 10 to 20 percent of the difference between African American and White American household wealth.[17]

Using the Health and Retirement Study (HRS) of 1992 Avery and Rendall estimated that only around one-tenth of African Americans reported receiving inheritances or substantial inter vivo transfers ($5,000 or more) compared to one-third of White Americans. In addition, the 1989 Survey of Consumer Finances (SCF) reported that the mean and median values of those money transfers were significantly higher for White American households: the mean was $148,578 households compared to $85,598 for African American households and the median was $58,839 to $42,478. The large differences in wealth in the parent-generations were a dominant factor in prediction the differences between African American and White American prospective inheritances.[18] Avery and Rendall used 1989 SCF data to discover that the mean value in 2002 of White Americans' inheritances was 5.46 times that of African Americans', compared to 3.65 that of current wealth. White Americans received a mean of $28,177 that accounted for 20.7% of their mean wealth while African Americans received a mean of $5,165 that accounted for 13.9% of their mean current wealth. Non-inherited wealth was more equally distributed than inherited wealth.[18]

Avery and Rendall found that family attributes favored White Americans when it came to factor influencing the amount of inheritances. African Americans were 7.3% less likely to have live parents, 24.5% more likely to have three or more siblings, and 30.6% less likely to be married or cohabiting (meaning there are two people who could gain inheritances to contribute to the household)[18] Keister discovered that large family size has a negative effect on wealth accumulation. These negative effects are worse for the poor and African Americans and Hispanics are more likely to be poor and have large families. More children also decrease the amount of gifts parents can give and the inheritance they leave behind for the children.[19]

Angel's research into inheritance showed that older Mexican American parents may give less financial assistance to their children than non-Hispanic White Americans because of their relatively high fertility rate so children have to compete for the available money. There are studies that indicate that elderly Hispanic parents of all backgrounds live with their adult children due to poverty and would choose to do otherwise if they had the resources to do so. African American and Latino families are less likely to financially aid adult children than non-Hispanic White families.[17]

Income effects

The racial wealth gap is visible in terms of dollar for dollar wage and wealth comparisons. For example, middle-class Blacks earn seventy cents for every dollar earned by similar middle-class Whites.[9]

Krivo and Kaufman found that information supporting the fact that increases in income does not affect wealth as much for minorities as it does for White Americans. For example, a $10,000 increase in income for White Americans increases their home equity $17,770 while the same increase only increase the home equities for Asians by $9,500, Hispanics by $15,150, and African Americans by $15,900.[20]

Financial decisions

Investments

Conley states that differences between African American and White American wealth begins because people with higher asset levels can take advantage of riskier investment instruments with higher rates of returns. Unstable income flows may lead to "cashing in" of assets or accumulation of debt over time, even if the time-averaged streams of income and savings are the same. African Americans may be less likely to invest in the stock market because they have a smaller parental head-start and safety net.[14]

Chong, Phillips and Phillips state that African Americans, Hispanics, and Asians invest less heavily in stocks than White Americans.[21] Hispanics and in some ways African Americans accumulate wealth slower than White Americans because of preference for near-term saving, favoring liquidity and low investment risk at the expense of higher yielding assets. These preferences may be due to low financial literacy leading to a lack of demand for investment services.[21] According to Lusardi, even though the stock market increased in value in the 1990s, only 6-7% of African Americans and Hispanics held stocks, so they did not benefit as much from the value increase.[13]

Use of financial services

The Federal Deposit Insurance Corporation in 2009 found that 7.7% of United States households are "unbanked". Minorities are more likely than White Americans to not have a banking account. 3.5% of Asians, 3.3% of White Americans, 21.7% of African Americans and 19.3% of Hispanics and 15.6% of remaining racial/ethnic categories do not have banking accounts.[21]

Lusardi's research revealed that education increases one's chances of having a banking account. A full high school education increases the chance of having a checking account by 15% compared to only an elementary education; having a parent with a high school education rather than only an elementary education increases one's chances of having a checking account by 2.8%. This difference in education level may explain the large proportion of "unbanked" Hispanics. The 2002 National Longitudinal Survey found that while only 3% of White Americans and 4% of African Americans had only an elementary education, close to 20% of Hispanics did and 43% of Hispanics had less than a high school education[13] Ibarra and Rodriguez believe that another factor that influences the Hispanic use of banking accounts is credit. Latinos are also more likely than White Americans or African Americans to have no or a thin credit history: 22% of Latinos have no credit score in comparison to 4% of White Americans and 3% of African Americans.[22]

Not taking other variables into account, Chong, Phillips, and Phillips survey of zip codes found that minority neighborhoods don't have the same access to financial planning services as White neighborhoods. There is also client segregation by investable assets. More than 80% of financial advisors prefer that clients have at least $100,000 in investable assets and more than 50% have a minimum asset requirement of $500,000 or above. Because of this, financial planning is possibly beyond the reach of those with low income, which comprises a large portion of African-Americans and Hispanics.[21] Fear of discrimination is another possible factor. Minorities may be distrustful of banks and lack of trust was commonly reported as why minorities, people with low education, and the poor chose not to have banking accounts.[13]

Poverty

There are large differences in poverty rates across racial groups. In 2009, the poverty rate was 9.9% for non-Hispanic Whites, 12.1% for Asians, 26.6% for Hispanics, and 27.4% for Blacks.[2] This data illustrates that Hispanics and Blacks experience disproportionately high percentages of poverty in comparison to non-Hispanics Whites and Asians. In discussing poverty, it is important to distinguish between episodic poverty and chronic poverty.

Episodic poverty

The U.S. Census Bureau defines episodic poverty as living in poverty for less than 36 consecutive months.[23] From the period between 2004 and 2006 the episodic poverty rate was 22.6% for non-Hispanic Whites, 44.5% for Blacks, and 45.8% for Hispanics.[23] Blacks and Hispanics experience rates of episodic poverty that are nearly double the rates of non-Hispanic Whites.

Chronic poverty

The U.S. Census Bureau defines chronic poverty as living in poverty for 36 or more consecutive months.[23] From the period between 2004 and 2006 the chronic poverty rate was 1.4% for non-Hispanic Whites, 4.5% for Hispanics, and 8.4% for Blacks.[23] Hispanics and Blacks experience much higher rates of chronic poverty when compared to non-Hispanic Whites.

Length of poverty spell

The U.S. Census Bureau defines length of poverty spell as the number of months spent in poverty. The median length of poverty spells was 4 months for non-Hispanic Whites, 5.9 months for Blacks, and 6.2 months for Hispanics.[23] The length of time spent in poverty varies by race. Non-Hispanic Whites experience the shortest length of poverty spells when compared to Blacks and Hispanics.

Housing

Home ownership

Home ownership is a crucial means by which families can accumulate wealth.[8] Over a period of time, homeowners accumulate home equity in their homes. In turn, this equity can contribute substantially to the wealth of homeowners. In summary, homeownership allows for the accumulation of home equity, a source of wealth, and provides families with insurance against poverty.[10] Ibarra and Rodriguez state that home equity is 61% of the net worth of Hispanic homeowners, 38.5% of the net worth of White homeowners, and 63% of the net worth of African-American homeowners.[22] Conley remarks that differences in rates of home ownership and housing value accrual may lead to lower net worth in the parental generation, which disadvantages the next.[14]

There are large disparities in homeownership rates by race. In 2010, the homeownership rate was 74.4% for non-Hispanic Whites, 58.9% for Asians or native Hawaiians/Pacific Islanders, 58.9% for American Indians/Alaskan natives, 47.5% for Hispanics, and 44.5% for Blacks.[24] From this data, non-Hispanic Whites own homes at a much higher rate that all other races, while Hispanics and Blacks own homes at much lower rates. This means that a high percentage of Hispanic and Black populations do not receive the benefits, such as wealth accumulation and insurance against poverty, that owning a home provides.

Home equity

There is a discrepancy in relation to race in terms of housing value. On average, the economic value of Black-owned units is 35% less than similar White-owned units. Thus, on average, Black-owned units sell for 35% less than similar White-owned units.[3] Krivo and Kaufman state that while median home value of White Americans is at least $20,000 more than that of African Americans and Hispanics, these differences are not a result of group differences in length of residences because Asians have the most equity on their homes but have lived in them for the shortest average period. African American and Hispanic mortgage holders are 1.5 to 2.5 times more likely to pay 9% or more on interest. Krivo and Kaufman calculate that the African-American/White gap in mortgage interest rates is 0.39%, which translates to a difference of $5,749 on the median home loan payment of a 30-year mortgage of a $53,882 home. The Hispanic/White gap (0.17%) translates to Hispanics paying $3,441 more on a 30-year mortgage on the median valued Hispanic home loan of $80,000. The authors conclude that the extra money could have been reinvested into wealth accumulation.[20]

Krivo and Kaufman also postulate that the types of mortgage loans minorities obtain contributes to the differences in home equity. FHA and VA loans make up one-third or more of primary loans for African Americans and Hispanics, while only 18% for White Americans and 16% for Asians. These loans require lower down payments and cost more than conventional mortgages, which contributes to a slower accumulation of equity. Asians and Hispanics have lower net equity on houses partly because they are youngest on average, but age has only a small effect on the Black-White gap in home equity. Previously owning a home can allow the homeowner to use money from selling the previous home to invest and increase the equity of later housing. Only 30% of African Americans in comparison to 60% of White Americas had previously owned a home. African-Americans, Asians, and Hispanics gain lower home equity returns in comparison to White Americans with increases in income and education.[20]

Residential segregation

Residential segregation can be defined as, "physical separation of the residential locations between two groups.[10] There are large discrepancies between races involving geographic location of residence. In the United States, poverty and affluence have become very geographically concentrated. Much residential segregation has been a result of the discriminatory lending practice of Redlining, which delineated certain, primarily minority race neighborhoods, as risky for investment or lending[25] The result has been neighborhoods with concentrated investment, and others neighborhoods where banks are less inclined to invest. Most notably, this geographic concentration of affluence and poverty can be seen in the comparison between suburban and urban populations. The suburbs have traditionally been primarily White populations, while the majority of urban inner city populations have traditionally been composed of racial minorities.[26] Results from the last few censuses suggest that more and more inner-ring suburbs around cities also are becoming home to racial minorities as their populations grow.

Education

In the United States, funding for public education relies greatly on local property taxes. Local property tax revenues may vary between different neighborhoods and school districts. This variance of property tax revenues amongst neighborhoods and school districts leads to inequality in education. This inequality manifests in the form of available school financial resources which provide educational opportunities, facilities, and programs to students.[4]

Returning to the concept of residential segregation, it is known that affluence and poverty have become both highly segregated and concentrated in relation to race and location.[26] Residential segregation and poverty concentration is most markedly seen in the comparison between urban and suburban populations in which suburbs consist of majority White populations and inner-cities consist of majority minority populations.[26] According to Barnhouse-Walters (2001), the concentration of poor minority populations in inner-cities and the concentration of affluent White populations in the suburbs, "is the main mechanism by which racial inequality in educational resources is reproduced."

Unemployment rates

In 2010, the unemployment rate was 7.5% for Asians, 8.7% for non-Hispanic Whites, 12.5% for Hispanics, and 16% for Blacks.[5] In terms of unemployment, it can be seen that there are two-tiers: relatively low unemployment for Asians and Whites, relatively high unemployment for Hispanics and Blacks.

Potential explanations

Several theories have been offered to explain the large racial gap in unemployment rates:

- Segregation and job decentralization

This theory argues that the effects of racial segregation pushed Blacks and Hispanics into the central city during a time period in which jobs and opportunities moved to the suburbs. This led to geographic separation between minorities and job opportunities which was compounded by struggles to commute to jobs in the suburbs due to lack of means of transportation. This ultimately led to high unemployment rates among minorities.[27]

- White gains

This theory argues that the reason minority disadvantage exists is because the majority group is able to benefit from it. For example, in terms of the labor force, each job not taken by a Black person could be job that gets occupied by a White person. This theory is based on the view that the White population has the most to gain from the discrimination of minority groups. In areas where there are large minority groups, this view predicts high levels of discrimination to occur for the reason that White populations stand to gain the most in those situations.[27]

- Job skill differentials

This theory argues that the unemployment disparity can be attributed to lower rates of academic success among minority groups (especially black Americans) leading to a lack of skills necessary for entering the modern work force.[27]

Crime rates and incarceration

In 2008, the prison population under federal and state correctional jurisdiction was over 1,610,446 prisoners. Of these prisoners, 20% were Hispanic (compared to 16.3% of the U.S. population that is Hispanic), 34% were White (compared to 63.7% of the U.S. population that is White), and 38% were Black (compared to 12.6% of the U.S. population that is Black).[6][28] Additionally, Black males were imprisoned at a rate 6.5 times higher than that of their White male counterparts.[6] According to a report by the National Council of La Raza, research obstacles undermine the census of Latinos in prison, and "Latinos in the criminal justice system are seriously undercounted. The true extent of the overrepresentation of Latinos in the system probably is significantly greater than researchers have been able to document.[29]

Consequences of a criminal record

After being released from prison, the consequences of having a criminal record are immense. Over 40 percent who are released will return to prison within the next few years. Those with criminal records who do not return to prison face significant struggles to find quality employment and income outcomes compared to those who do not have criminal records.[30]

Potential causes

- Poverty

A potential cause of such disproportionately high incarceration rates for Black Americans is that Black Americans are disproportionately poor.[31] Conviction is a crucial part of the process that leads to either guilt or innocence. There are two important factors that play a role in this part of the process: the ability to make bail and the ability to access high-quality legal council. Due to the fact that both of these important factors cost money, it is unlikely that poor Black Americans are able to afford them and benefit from them.[31] Sentencing is another crucial part of the process that determines how long individuals will remain incarcerated. Several sociological studies have found that poor offenders receive longer sentences for violent crimes and crimes involving drug use, unemployed offenders are more likely to be incarcerated than their employed counterparts, and then even with similar crimes and criminal records minorities were imprisoned more often than Whites.[31]

- Racial profiling

Racial profiling is defined as,"any police-initiated action that relies on the race, ethnicity, or national origin, rather than the behavior of an individual or information that leads the police to a particular individual who has been identified as being, or having been, engaged in criminal activity."[32] Another potential cause for the disproportionately high incarceration rates of Blacks and Hispanics is that racial profiling occurs at higher rates for Blacks and Hispanics. Eduardo Bonilla-Silva states that racial profiling can perhaps explain the over representation of Blacks and Hispanics in U.S. prisons[3]

- Racial segregation

"Racial residential segregation is a fundamental cause of racial disparities in health".[33] Racial segregation can result in decreased opportunities for minority groups in income, education, etc. While there are laws against racial segregation, study conducted by D. R. Williams and C. Collins focuses primarily on the impacts of racial segregation, which leads to differences between races.

See also

- African-American Civil Rights Movement (1955–1968)

- Chinese Exclusion Act

- Glass ceiling

- Immigration Act of 1924

- Indian Appropriations Act

- Japanese American internment

- Native Americans and reservation inequality

- Racial achievement gap in the United States

- Racial segregation in the United States

- Racial wage gap in the United States

- Racism in the United States

- Mexican Repatriation

- Operation Wetback

- Segregation in the United States

- Sociology of race and ethnic relations

- The New Jim Crow

References

- 1 2 3 Shapiro, Thomas M. (2004). The Hidden Cost of Being African American. New York: Oxford UP. p. 33. ISBN 978-0-19-518138-8.

- 1 2 DeNavas-Wait, Carmen; Bernadette D. Proctor; Jessica C. Smith. "Income, Poverty, and Health Insurance Coverage in the United States:2009" (PDF). Current Population Reports. U.S. Census Bureau. p. 15. Retrieved 18 October 2011.

- 1 2 3 4 5 6 7 8 9 10 Bonilla-Silva, Eduardo (2003). Racism without Racists: Color-blind Racism and the Persistence of Racial Inequality in the United States. Lanham: Rowman & Littlefield. pp. 2–29. ISBN 978-0-7425-1633-5.

- 1 2 Barnhouse Walters, Pamela (2001). "Educational Access and the State: Historical Continuities and Discontinuities in Racial Inequality in American Education". Sociology of Education. 74: 35–49. doi:10.2307/2673252. JSTOR 2673252.

- 1 2 "Unemployed Workers-Summary: 1990-2010" (PDF). Labor Force, Employment, & Earnings. U.S. Census Bureau. Retrieved 18 October 2011.

- 1 2 3 Sabol, William J.; Heather C. West; Matthew Cooper. "Prisoners in 2008" (PDF). Bureau of Justice Statistics: Bulletin. U.S. Department of Justice. Retrieved 18 October 2011.

- ↑ "Tackling Ethnic and Regional Inequalities" (PDF). Combating Poverty and Inequality: Structural Change, Social Polics, and Politi. United Nations Research Institute for Social Development. Retrieved 18 October 2011.

- 1 2 3 Thomas Shapiro; Tatjana Meschede; Sam Osoro (February 2013). "The Roots of the Widening Racial Wealth Gap: Explaining the Black-White Economic Divide" (PDF). Research and Policy Brief. Brandeis University Institute on Assets and Social Policy. Retrieved 16 March 2013. External link in

|publisher=(help) - 1 2 Oliver, Melvin L.; Thomas M. Shapiro (2006). Black Wealth, White Wealth: a New Perspective on Racial Inequality. New York: Routledge. pp. 2–7. ISBN 978-0-415-95167-8.

- 1 2 3 Danzinger, Shelton H. (2001). Robert H. Haveman, ed. Understanding Poverty. New York: Russel Sage Foundation. pp. 359–391. ISBN 978-0-674-00876-2. Retrieved 11 October 2013.

Housing Discrimination and Residential Segregation as Causes of Poverty

- 1 2 3 4 5 6 Kochhar, Rakesh; Fry, Richard; Taylor, Paul (July 26, 2011). "Wealth Gaps Rise to Record Highs Between Whites, Blacks, Hispanics: Twenty-to-One". Pew Research Center. Retrieved 15 April 2012.

- ↑ Moore, Antonio (November 10, 2015). "Only 5% of African American Households Have More than $350,000 in Net Worth". Eurweb. Retrieved 11 November 2015.

- 1 2 3 4 5 6 Lusardi, Annamaria (2005). "Financial Education and the Saving Behavior of African American and Hispanic Households" (PDF). Report for the US Department of Labor. Retrieved 26 March 2012.

- 1 2 3 4 5 6 Conley, Dalton (2010). Being Black, Living in the Red: Race, Wealth, and Social Policy in America. Berkeley, California: University of California Press.

- ↑ Bowles, Samuel; Gintis, Herbert (2002). "The Inheritance of Inequality". Journal of Economic Perspectives. 16 (3): 3–30. doi:10.1257/089533002760278686.

- ↑ Bowman, Scott W. (2011). "Multigenerational Interactions in Black Middle Class Wealth and Asset Decision Making". Journal of Family Economic Issues. 32 (1): 15–26. doi:10.1007/s10834-010-9204-5.

- 1 2 Angel, Jacqueline L. (2008). Inheritance in Contemporary America. Baltimore Maryland: The Johns Hopkins University Press.

- 1 2 3 Avery, Robert B.; Rendall, Michael S. (2002). "Lifetime Inheritances of Three Generations of Whites and Blacks". American Journal of Sociology. 107 (5): 1300–1346. doi:10.1086/344840.

- ↑ Keister, Lisa A. (2002). "Race, Family Structure, and Wealth: The Effect of Childhood Family on Adult Assets". Sociological Perspectives. 47 (2): 161–187.

- 1 2 3 Krivo, Lauren J.; Kaufman, Robert L. (2004). "Housing and Wealth Inequality: Racial-Ethnic Differences in Home Equity in the United States". Demography. 41 (3): 585–605. doi:10.1353/dem.2004.0023.

- 1 2 3 4 Chong, James; Phillips, Lynn; Phillips, Michael (2011). "The Impact of Neighborhood Ethnic Composition on Availability of Financial Planning Services". Journal of Financial Service Professionals. 65 (6): 71–83.

- 1 2 Ibarra, Beatriz; Rodriguez, Erik (2006). "Closing The Wealth Gap: Eliminating Structural Barriers To Building Assets In The Latino Community". Harvard Journal of Hispanic Policy. 18: 25–38.

- 1 2 3 4 5 Anderson, Robin J. "Dynamics of Economic Well-Being: 2004-2006 Poverty" (PDF). Household Economic Studies. U.S. Census Bureau. Retrieved 25 October 2011.

- ↑ "Homeownership Rates by Race and Ethnicity of Householder: 1994-2010". Housing Vacancies and Homeownership: Annual Statistics 2010. U.S. Census Bureau. Retrieved 18 October 2011.

- ↑ Hallahan, Kirk. "THE MORTGAGE REDLINING CONTROVERSY, 1972-1975". Qualitative Studies Division, Association in Journalism and Mass Communication, Montreal August 1992. Retrieved 12 November 2012.

- 1 2 3 Douglass S. Massey (2004). "The New Geography of Inequality in Urban America". In Henry, C. Michael. Race, Poverty, and Domestic Policy. New Haven: Yale University Press. pp. 173–187. ISBN 978-0-300-12984-7.

- 1 2 3 Farley, John E. (1987). "Disproportionate Black and Hispanic Unemployment in U.S. Metropolitan Areas: The Roles of Racial Inequality, Segregation and Discrimination in Male Joblessness". Journal of Economics and Sociology. 46 (2): 129–150. doi:10.1111/j.1536-7150.1987.tb01949.x.

- ↑ "USA QuickFacts from the U.S. Census Bureau". 2010 Census. U.S. Census Bureau. Retrieved 4 September 2012.

- ↑ SpearIt (2015-04-02). "How Mass Incarceration Underdevelops Latino Communities". Rochester, NY: Social Science Research Network.

- ↑ Pager, Devah (March 2003). "The Mark of a Criminal Record" (PDF). The American Journal of Sociology. 108 (5): 325–363. doi:10.1086/374403.

- 1 2 3 Gallagher, Charles A. (2009). Rethinking the Color Line: Readings in Race and Ethnicity. Boston: McGraw-Hill. pp. 192–203. ISBN 978-0-07-340427-1.

... and the Poor Get Prison

- ↑ Risse, Mathias; Richard Zechauser (April 2004). "Racial Profiling". Philosophy and Public Affairs. 32 (2): 131–170. doi:10.1111/j.1088-4963.2004.00009.x. Retrieved 11 October 2013.

- ↑ Williams,Collins

- Williams, DR; Collins, C (2001). "Racial residential segregation: a fundamental cause of racial disparities in health". Public Health Rep. 116: 404–16. doi:10.1093/phr/116.5.404. PMC 1497358

. PMID 12042604.

. PMID 12042604.