Call option

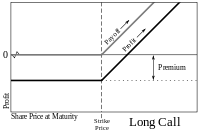

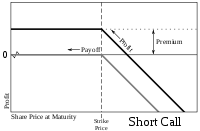

A call option, often simply labeled a "call", is a financial contract between two parties, the buyer and the seller of this type of option.[1] The buyer of the call option has the right, but not the obligation, to buy an agreed quantity of a particular commodity or financial instrument (the underlying) from the seller of the option at a certain time (the expiration date) for a certain price (the strike price). The seller (or "writer") is obligated to sell the commodity or financial instrument to the buyer if the buyer so decides. The buyer pays a fee (called a premium) for this right.

When you buy a call option, you are buying the right to buy a stock at the strike price, regardless of the stock price in the future before the expiration date. Conversely, you can short or "write" the call option, giving the buyer the right to buy that stock from you anytime before the option expires. To compensate you for that risk taken, the buyer pays you a premium, also known as the price of the call. The seller of the call is said to have shorted the call option, and keeps the premium (the amount the buyer pays to buy the option) whether or not the buyer ever exercises the option.

For example, if a stock trades at $50 right now and you buy its call option with a $50 strike price, you have the right to purchase that stock for $50 regardless of the current stock price as long as it has not expired. Even if the stock rises to $100, you still have the right to buy that stock for $50 as long as the call option has not expired. Since the payoff of purchased call options increases as the stock price rises, buying call options is considered bullish. When the price of the underlying instrument surpasses the strike price, the option is said to be "in the money". On the other hand, If the stock falls to below $50, the buyer will never exercise the option, since he would have to pay $50 per share when he can buy the same stock for less. If this occurs, the option expires worthless and the option seller keeps the premium as profit. Since the payoff for sold (or written) call options increases as the stock price falls, selling call options is considered bearish.

All call options have the following three characteristics:

- Strike price: this is the price at which you can buy the stock (if you have bought a call option) or the price at which you must sell your stock (if you have sold a call option).

- Expiry date: this is the date on which the option expires, or becomes worthless, if the buyer doesn't exercise it.

- Premium: this is the price you pay when you buy an option and the price you receive when you sell an option.

The initial transaction in this context (buying/selling a call option) is not the supplying of a physical or financial asset (the underlying instrument). Rather it is the granting of the right to buy the underlying asset, in exchange for a fee — the option price or premium.

Exact specifications may differ depending on option style. A European call option allows the holder to exercise the option (i.e., to buy) only on the option expiration date. An American call option allows exercise at any time during the life of the option.

Call options can be purchased on many financial instruments other than stock in a corporation. Options can be purchased on futures or interest rates, for example (see interest rate cap), and on commodities like gold or crude oil. A tradeable call option should not be confused with either Incentive stock options or with a warrant. An incentive stock option, the option to buy stock in a particular company, is a right granted by a corporation to a particular person (typically executives) to purchase treasury stock. When an incentive stock option is exercised, new shares are issued. Incentive options are not traded on the open market. In contrast, when a call option is exercised, the underlying asset is transferred from one owner to another.

Example of a call option on a stock

An investor typically 'buys a call' when he expects the price of the underlying instrument will go above the call's 'strike price,' hopefully significantly so, before the call expires. The investor pays a non-refundable premium for the legal right to exercise the call at the strike price, meaning he can purchase the underlying instrument at the strike price. Typically, if the price of the underlying instrument has surpassed the strike price, the buyer pays the strike price to actually purchase the underlying instrument, and then sells the instrument and pockets the profit. Of course, the investor can also hold onto the underlying instrument, if he feels it will continue to climb even higher.

An investor typically 'writes a call' when he expects the price of the underlying instrument to stay below the call's strike price. The writer (seller) receives the premium up front as his or her profit. However, if the call buyer decides to exercise his option to buy, then the writer has the obligation to sell the underlying instrument at the strike price. Often the writer of the call does not actually own the underlying instrument, and must purchase it on the open market in order to be able to sell it to the buyer of the call. The seller of the call will lose the difference between his purchase price of the underlying instrument and the strike price. This risk can be huge if the underlying instrument skyrockets unexpectedly in price.

- The current price of ABC Corp stock is $45 per share, and investor 'Greg R.' expects it will go up significantly. Greg buys a call contract for 100 shares of ABC Corp from 'Terence R.,' who is the call writer/seller. The strike price for the contract is $50 per share, and Greg pays a premium up front of $5 per share, or $500 total. If ABC Corp does not go up, and Greg does not exercise the contract, then Greg has lost $500.

- ABC Corp stock subsequently goes up to $60 per share before the contract expires. Greg exercises the call option by buying 100 shares of ABC from Terence for a total of $5,000. Greg then sells the stock on the market at market price for a total of $6,000. Greg has paid a $500 contract premium plus a stock cost of $5,000, for a total of $5,500. He has earned back $6,000, yielding a net profit of $500.

- If, however, the ABC stock price drops to $40 per share by the time the contract expires, Greg will not exercise the option (i.e., Greg will not buy a stock at $50 per share from Terence when he can buy it on the open market at $40 per share). Greg loses his premium, a total of $500. Terence, however, keeps the premium with no other out-of-pocket expenses, making a profit of $500.

- The break-even stock price for Greg is $55 per share, i.e., the $50 per share for the call option price plus the $5 per share premium he paid for the option. If the stock reaches $55 per share when the option expires, Greg can recover his investment by exercising the option and buying 100 shares of ABC Corp stock from Terence at $50 per share, and then immediately selling those shares at the market price of $55. His total costs are then the $5 per share premium for the call option, plus $50 per share to buy the shares from Greg, for a total of $5,500. His total earnings are $55 per share sold, or $5,500 for 100 shares, yielding him a net $0. (Note that this does not take into account broker fees or other transaction costs.) Note, however, that the $5 per share premium is a sunk cost that he has already paid regardless of whether he chooses to exercise the call. Thus, while he breaks even at $55 per share, actually, he makes a $5 per share profit that covers the earlier expense of $5 per share. Thus it is in his interest to exercise the call if the price goes above $50, even if it does not reach $55, because the profit he makes will reduce his net loss.

Example of valuing a stock option

A company issues an option for the right to buy their stock. An investor buys this option and hopes the stock goes higher so their option will increase in value.

- Theoretical option price = (current price + theoretical time/volatility premium) – strike price

Let's look at an actual example, PNC options for January 2012:

- Strike price – the price the investor can buy the stock at through the option.

- Symbol – like a stock symbol but for options it incorporates the date.

- Last – like the last stock price, it is the last price traded between two parties.

- Change – how much it went up and down today.

- Bid – what a person is bidding for the option.

- Ask – what someone wants to sell the option for.

- Vol – how many options traded today.

- Open Int – how many options are available, i.e. the option float

Notes:

- The bid/ask price is more relevant in ascertaining the value of the option than the last price since options are not frequently traded. Meaning the value is usually the Ask/Bid Price.

- An option usually covers 100 shares. So the bid/ask price is multiplied by 100 to get the total cost.

Let's say we bought 3 PNC strike $45, January 2012 call options in August for $11.75. That means we paid $3,525 (11.75 * 3 options for 100 shares each) for the right to buy 300 (3*100) PNC shares for $45 per share between now and January 2012.

The stock at that time traded at $50.65 meaning the theoretical call premium was $6.1 as shown by our formula: (current price + theoretical time/volatility premium) – strike price, (50.65 + 6.1 – 45 = 11.75).

Today the stock is trading at $64 making the call option worth $19.45 with a theoretical call premium now of 45 cents above its in-the-money intrinsic value $19 (the $64 market price minus the call option $45 strike price). The call premium tends to go down as the option gets closer to the call date. And it goes down as the option price rises relative to the stock price, i.e. the 19.45 the option is now worth 30% (19.45/ $64) of the price per PNC shares. In August it was 23% (11.75/$50.65). The lower percentage of the option's price is based on the stock's price, the more upside the investor has, therefore the investor will pay a premium for it.

This option could be used to buy 300 PNC shares today at $45, it can be sold on the option market for $19.45 or for $5,835 (19.45 * 3 options for 100 shares each). Or it can be held as the investor bets that the price will continue to increase. The investor must make a decision by January 2012: he will either have to sell the option or buy the 300 shares. If the stock price drops below the strike price on this date the investor will not exercise his right since it will be worthless.

Price of options

Option values vary with the value of the underlying instrument over time. The price of the call contract must reflect the "likelihood" or chance of the call finishing in-the-money. The call contract price generally will be higher when the contract has more time to expire (except in cases when a significant dividend is present) and when the underlying financial instrument shows more volatility. Determining this value is one of the central functions of financial mathematics. The most common method used is the Black–Scholes formula. Importantly, the Black-Scholes formula provides an estimate of the price of European-style options.[2]

Whatever the formula used, the buyer and seller must agree on the initial value (the premium or price of the call contract), otherwise the exchange (buy/sell) of the call will not take place.

Adjustment to Call Option: When a call option is in-the-money i.e. when the buyer is making profit, he has many options. Some of them are as follows:

- He can sell the call and book his profit

- If he still feels that there is scope of making more money he can continue to hold the position.

- If he is interested in holding the position but at the same time would like to have some protection,he can buy a protective "put" of the strike that suits him.

- He can sell a call of higher strike price and convert the position into "call spread" and thus limiting his loss if the market reverses.

Similarly if the buyer is making loss on his position i.e. the call is out-of-the-money, he can make several adjustments to limit his loss or even make some profit.

Call Option Profit / Loss Chart

Trading options involves a constant monitoring of the option value, which is affected by the following factors:

- Changes in the base asset price (the higher the price, the more expensive the call option is)

- Changes in the volatility of the base asset (the higher the volatility, the more expensive the call option is)

- Time decay – as time goes by, options become cheaper and cheaper.

Moreover, the dependence of the option value to price, volatility and time is not linear – which makes the analysis even more complex.

One very useful way to analyze and track the value of an option position is by drawing a Profit / Loss chart that shows how the option value changes with changes in the base asset price and other factors. For example, this Profit / Loss chart shows the profit / loss of a call option position (with $100 strike and maturity of 30 days) purchased at a price of $3,5 (blue graph – the day of the purchase of the option; orange graph – at expiry):

Options

- Put option

- Binary option

- Bond option

- Credit default option

- Exotic option

- Foreign exchange option

- Interest rate cap and floor

- Options on futures

- Stock option

- Swaption

See also

References

|