Normal good

In economics, normal goods are any goods for which demand increases when income increases, and falls when income decreases but price remains constant, i.e. with a positive income elasticity of demand.[1][2] The term does not necessarily refer to the quality of the good, but an abnormal good would clearly not be in demand, except for possibly lower socioeconomic groups.

In particular, when the price of a normal good is zero, the demand is infinite.

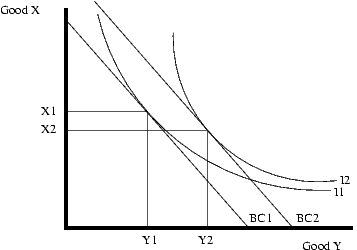

Depending on the indifference curves, the amount of a good bought can either increase, decrease, or stay the same when income increases. In the diagram below, good Y is a normal good since the amount purchased increases from Y1 to Y2 as the budget constraint shifts from BC1 to the higher income BC2. Good X is an inferior good since the amount bought decreases from X1 to X2 as income increases.

Examples include Holidays, Cars, diamonds, branded fashions, hi-tech products etc.