Economy of Europe

The economy of Europe comprises more than 731 million people in 48 different countries. Like other continents, the wealth of Europe's states varies, although the poorest are well above the poorest states of other continents in terms of GDP and living standards. The difference in wealth across Europe can be seen roughly in former Cold War divide, with some countries breaching the divide (Greece, Portugal, Slovenia and the Czech Republic). Whilst most European states have GDP per capita higher than the world's average and are very highly developed (Liechtenstein, Luxembourg, Monaco, Andorra, Norway, Sweden, the Netherlands, Switzerland), some European economies, despite their position over the world's average (except for Moldova) in the Human Development Index (Albania, Armenia, Azerbaijan, Bosnia and Herzegovina, Georgia, Macedonia, Kosovo, Belarus, Ukraine) are still catching up with European leading countries.

Throughout this article "Europe" and derivatives of the word are taken to include selected states whose territory is only partly in Europe – such as Turkey (depending on a definition – whole country or just Thrace), Azerbaijan (Caucasus), and the Russian Federation (its European part to Ural Mountains) – and states that are geographically in Asia, bordering Europe and culturally adherent to the continent – such as Armenia, Georgia, and Cyprus.

Europe in 2010 had a nominal GDP of $19.920 trillion[1] (30.2% of the world). Europe's largest national economy is that of Germany, which ranks fourth globally in nominal GDP, and fifth in purchasing power parity (PPP) GDP;[2] followed by the United Kingdom, ranking fifth globally in nominal GDP, followed by France, ranking sixth globally in nominal GDP, followed by Italy, which ranks seventh globally in nominal GDP, followed by Russia ranking tenth globally in nominal GDP then by Spain ranking thirteenth globally in nominal GDP.[3]

These 6 countries all rank in the world's top 15, therefore European economies account for half of the 10 wealthiest ones. The end of World War II brought European countries closer together, culminating in the formation of the European Union (EU) and in 1999, the introduction of a unified currency – the euro. The EU as a whole is the wealthiest and largest economy in the world, topping the US by more than 2,000 billion at a time of great economic slowdown– see List of countries by GDP. In 2009 Europe remained the world's wealthiest region. Its $33 trillion in assets under management represented more than one-third of the world's wealth. Unlike North America ($29,3 trillion) it was one of few regions where wealth surpassed its precrisis year-end peak.[4]

Of the top 500 largest corporations measured by revenue (Fortune Global 500 in 2010), 184 have their headquarters in Europe. 161 are located in the EU, 15 in Switzerland, 6 in Russia, 1 in Turkey, 1 in Norway.[5]

As noted by the Spanish sociologist Manuel Castells the average standard of living in Western Europe is very high.

"The bulk of the population in Western Europe still enjoys the highest living standards in the world, and in the world's history."[6]

Economic development

Pre-1945: Industrial growth

Prior to World War II, Europe's major financial and industrial states were the United Kingdom, France and Germany. The Industrial Revolution, which began in Britain, had spread rapidly across Europe, and before long the entire continent was at a high level of industry. World War I had briefly led to the industries of some European states stalling, but in the run-up to World War II Europe had recovered well, and was competing with the ever increasing economic might of the United States of America.

However, World War II caused the destruction of most of Europe's industrial centres, and much of the continent's infrastructure was laid to waste.

1945–1990: The Cold War era

Following World War II, European Government was in tatters. Many non-Socialist European governments moved to link their economies, laying the foundation for what would become the European Union. This meant a huge increase in shared infrastructure and cross-border trade. Whilst these European states rapidly improved their economies, by the 1980s, the economy of the COMECON was struggling, mainly due to the massive cost of the Cold War. The GDP and the living standards of Central and Eastern European states were lower than in other parts of Europe. Even free-market Greece, situated in South-Eastern Europe, struggled due to geographical isolation from non-socialist part of Europe.

The European Community grew from 6 original members following World War II, to 12 in this period.

Average living standards in Europe rose significantly during the post-war period, as characterised by these findings:[7]

Per capita private consumption (PPSs) in 1980

- Luxembourg: 5495

- France: 5395

- Germany, Federal Republic: 5319

- Belgium: 5143

- Denmark: 4802

- Netherlands: 4792

- United Kingdom: 4343

- Italy: 4288

- Ireland: 3029

Per capita personal disposable income (PPSs) in 1980

- Belgium: 6202

- France: 6044

- Germany, Federal Republic: 5661

- Netherlands: 5490

- Italy: 5378

- Denmark: 4878

- United Kingdom: 4698

Rise of the European Union

When the 'Eastern Bloc' dissolved around 1991, these states struggled to adapt to free-market systems. There was, however, a huge variation in degrees of success, with Central European states such as the Czech Republic, Hungary, Slovakia, Slovenia and Poland adapting reasonably quickly, whilst states that used to form the USSR such as Russia, Belarus and Ukraine struggled to reform their crumbling infrastructures.

Many developed European countries were quick to develop economic ties with fellow European states, where democracy was reintroduced. After the Revolutions of 1989, states in Central Europe and the Baltic states dealt with change, former Yugoslavian republics descended into war and Russia, Ukraine and Belarus are still struggling with their old systems.

Europe's largest economy, Germany, struggled upon unification in 1991 with former communist German Democratic Republic, or East Germany, influenced by the Soviet Union. GDR, had much of its industrial infrastructure removed during the Cold War, and for many years unified Germany struggled to build infrastructure in the former East Germany up to the level of former West Germany.

Peace did not come to Yugoslavia for a decade, and by 2003, there were still many NATO and EU peacekeeping troops present in Bosnia and Herzegovina, Macedonia, and Kosovo[a] . War severely hampered economic growth, with only Slovenia making any real progress in the 1990s.

European economy was affected by September 11 Attacks in United States in 2001, Germany, Switzerland, France, and United Kingdom was hardest. But, in 2002/2003, the Economy began to recover from attacks in US.

The economy of Europe was by this time dominated by the EU, a huge economic and political organization with then 15 of Europe's states as full members. EU membership was seen as something to aspire to, and the EU gave significant support and aid to those Central and Eastern European states willing to work towards achieving economies that met the entry criteria. During this time, 12 of the 15 members of the EU became part of the Eurozone, a currency union launched in 1999, whereby each member uses a shared currency, the Euro, which replaced their former national currencies. Three states chose to remain outside the Eurozone and continue with their own currencies, namely Denmark, Sweden and the United Kingdom.

2004–2007: EU expansion

In early 2004, 10 mostly former communist states joined the EU in its biggest ever expansion, enlarging the union to 25 members, with another eight making associated trade agreements. The acceding countries are bound to join the Eurozone and adopt the common currency Euro in the future. The process includes the European Exchange Rate Mechanism, of which some of these countries are already part.

Most European economies are in very good shape, and the continental economy reflects this. Conflict and unrest in some of the former Yugoslavia states and in the Caucasus states are hampering economic growth in those states, however.

In response to the massive EU growth, in 2005 the Russian-dominated Commonwealth of Independent States (CIS) created a rival trade bloc to the EU, open to any previous USSR state, (including both the European and Asian states). 12 of the 15 signed up, with the three Baltic states deciding to align themselves with the EU. Despite this, the three Caucasus states have said in the past they would one day consider applying for EU membership, particularly Georgia. This is also true of Ukraine since the Orange Revolution.

2008-present: Eurozone expansion and European debt crisis

Slovenia became the first formerly communist nation to adopt the EU currency, the euro, in 2007, followed by Malta and Cyprus in 2008, Slovakia in 2009, Estonia in 2011 and Latvia in 2014 as the 18th member state to enter the eurozone, despite initially significant opposition among the citizens in the nation to continue the major currency transition. On the 23rd of July 2014, the Council of the European Union confirmed Lithuania to be the latest EU member to join the eurozone by the start of 2015. Recently, Croatia became the 28th member of the European Union, which had entered on the 1st day of July 2013.

In 2008, the Global Financial Crisis, triggered by the housing bubble in the United States, caused a significant decline in the GDP of the majority of the European economies, which was a precedent to a far more broader and problematic Eurozone debt crisis, which threatened the collapse of economies in the south, particularly Italy, recently affected by the ongoing political crisis, and Portugal and Spain. Ireland and Greece are also hit hard, with Ireland exiting the crisis in mid-2013. Meanwhile, increased bailouts of the International Monetary Fund and European Central Bank alleviated somehow the situation in the debt-stricken nations, with Central and East European economies led by Germany escaping the worst of the 2010s debt crisis.

By the mid 2010s, 2014–2015, Ireland was recovering at a steady pace having graduated from the bail out programme successfully. The Eurozone as a whole had become more stable, however problems in Greece and slow recovery in Italy and in Iberia (Spain and Portugal) continue in keeping growth in the Euro area to a minimum. Germany continues to lead Europe in stability and growth, while both the UK and Ireland are seeing strong growth of 3–4%. Unemployment in Ireland reducing at the fastest levels in Europe, expected to reach 8% by 2016, down from double that in 2011. Growth outlook in general remains opimistic for Europe in the future. With positive growth expected across the Euro area. All though uncertainty still surrounds Greece and debt payments in the Greek state, at present things appear stable.

Regional variation

European countries with a long history of trade, a free market system, and a high level of development in the previous century are generally in the north and west of the continent. They tend to be wealthier and more stable than countries congregated in European east and south, even though the gap is converging, especially in Central and Eastern Europe, due to higher growth rates.

The poorest states are those that just emerged from communism, fascist dictatorships and civil wars, namely those of the former Soviet Union and Yugoslavia, excluding Slovenia. Former Western Bloc itself presents some living standards and development differences, with the greatest contrast seen between Scandinavia (Sweden, Norway, Denmark, Finland) and Spain, Portugal, Italy and Greece.

Below is a map of European countries by gross national income per capita.[8] High income in blue ($12,616 or more, as defined by the World Bank), upper middle income in green ($4,086 – $12,615) and lower middle income ($1,036 – $4,085) in yellow.

Cities by GDP

| Rank | City | State | GDP in $ID B | Population M (LUZ) | GDP per capita $ID K | Eurozone |

|---|---|---|---|---|---|---|

| 1 | London | |

$732 | 11.9 | $61.5 | N |

| 2 | Paris | |

$669 | 11.5 | $62.4 | Y |

| 3 | Moscow | |

$520 | 11.5 | $45.2 | N |

| 4 | Madrid | |

$230 | 5.80 | $39.7 | Y |

| 5 | Barcelona | |

$177 | 4.97 | $35.6 | Y |

| 6 | Rome | |

$144 | 3.46 | $41.6 | Y |

| 7 | Milan | |

$136 | 3.08 | $44.2 | Y |

| 8 | Vienna | |

$122 | 2.18 | $56.0 | Y |

| 9 | Lisbon | |

$98 | 2.44 | $40.2 | Y |

| 10 | Athens | |

$96 | 4.01 | $23.9 | Y |

| 11 | Berlin | |

$95 | 4.97 | $19.1 | Y |

European Union

The European Union has the largest economy in the world. Trade within the Union accounts for more than one-third of the world total.

The European Union or EU is a supranational union of 28 European states, the most recent acceding member being Croatia, which became full member on 1 July 2013. It has many functions, the most important being the establishment and maintenance of a common single market, consisting of a customs union, a single currency (adopted by 18 of the 28 member states[9]), a Common Agricultural Policy and a Common Fisheries Policy. The European Union also undertakes various initiatives to co-ordinate activities of the member states.

The union has evolved over time from a primarily economic union to an increasingly political one. This trend is highlighted by the increasing number of policy areas that fall within EU competence: political power has tended to shift upwards from the Member States to the EU.

European Free Trade Association

The European Free Trade Association (EFTA) was established on 3 May 1960 as an alternative for European states that did not wish to join the European Union, creating a trade bloc with fewer central powers.

The EFTA member states as of 1992 were Austria, Denmark, Finland, Iceland, Liechtenstein, Norway, Sweden and Switzerland. In 2014 only four ountries, Iceland, Norway, Switzerland and Liechtenstein, remained members of EFTA, as the other members have gradually left to join the EU.

European Economic Area

The European Economic Area (EEA) came into being on 1 January 1994 following an agreement between the European Free Trade Association (EFTA) and the European Union (EU). It was designed to enable EFTA countries to participate in the European Single Market without having to join the EU.

In a referendum, Switzerland (ever keen on neutrality) chose not to participate in the EEA (although it is linked to the European Union by bilateral agreements similar in content to the EEA agreement), so the current members are the EU states plus Norway, Iceland and Liechtenstein.

A Joint Committee consisting of the non EU members plus the European Commission (representing the EU) has the function of extending relevant EU Law to the non EU members.

Commonwealth of Independent States

The Commonwealth of Independent States (CIS) is a confederation consisting of 9 of the 15 states of the former Soviet Union, (the exceptions being the three Baltic states, Georgia, Turkmenistan, and Ukraine (Turkmenistan and Ukraine are participating states in the CIS)). Although the CIS has few supranational powers, it is more than a purely symbolic organization and possesses co-ordinating powers in the realm of trade, finance, lawmaking and security. The most significant issue for the CIS is the establishment of a full-fledged free trade zone / economic union between the member states, to be launched in 2005. It has also promoted co-operation on democratization and cross-border crime prevention.

Central European Free Trade Agreement

The Central European Free Trade Agreement (CEFTA) is a trade bloc of: Albania, Bosnia and Herzegovina, Macedonia, Moldova, Montenegro, Serbia and the United Nations Interim Administration Mission in Kosovo (UNMIK) on behalf of Kosovo.

Currency and central banks

The most common currency within Europe is the euro, the currency of the European Union. To join, each new EU member must meet certain criteria, when these are met their own currencies will be replaced by the euro. Becoming a member of the EU involves a pledge to work towards Eurozone membership, (except in the cases of the United Kingdom and Denmark who have opt-outs). Currently, 17 of the 28 EU member states use the euro. Each EU member's central bank is part of the European System of Central Banks, and in addition, those that use the euro are part of the European Union's central bank, the European Central Bank.

There are some non-EU members who have elected to use the euro as their national currency, either with or without specific agreements with the EU to do so, (those with agreements with the EU may mint their own euro coins). The French overseas territories and departments of Mayotte and Réunion in the Indian Ocean, Guadeloupe and Martinique in the Caribbean and French Guiana in South America all use the euro, among many other islands in the Pacific, Caribbean and indeed around the globe that are ruled directly by European countries.

Some countries while maintaining their own national currency have pegged its value to the euro. In some of these countries, there is a fixed exchange rate between the national currency and the euro and in this case the currency is actually a submultiple of the euro. In other countries, the national currency's value fluctuates within a band (generally 15%) around a set rate. Currencies pegged to the euro include the currencies of Bulgaria, Bosnia and Herzegovina and Cape Verde. Denmark has a foreign exchange band tied to the euro.

The CIS is also planning to introduce a single currency among its members.

Below is a list of the central banks and currencies of Europe, with exchange rates between each currency and both the euro and US dollars as of 1 May 2010.

Table as of 21 November 2010.

Stock exchanges

As of May 1, 2010, five (5) European cities are ranking among the 10 largest financial centers in the world: London (1st), Paris (5th), Frankfurt (6th), Zurich (7th) and Geneva (8th).

There are many stock exchanges within Europe.

- Pan-European:

- Albania:

- Tirana Stock Exchange (TSE)

- Austria:

- Belgium:

- Bosnia and Herzegovina

- Bulgaria:

- Croatia:

- Cyprus:

- Cyprus Stock Exchange (CSE)

- Czech Republic:

- Prague Stock Exchange (PSE)

- Denmark:

- Copenhagen Stock Exchange (KFX) (part of OMX)

- Estonia:

- Tallinn Stock Exchange (part of OMX)

- Faroe Islands:

- Faroese Securities Market, in cooperation with Iceland Stock Exchange

- Finland:

- Helsinki Stock Exchange (part of OMX)

- France:

- Euronext Paris ("La Bourse de Paris") (CAC40)

- Georgia

- Georgian Stock Exchange (GSE)

- Germany:

- Frankfurt Stock Exchange (part of Deutsche Börse) (DAX)

- Greece:

- Athens Stock Exchange (General)

- Hungary:

- Budapest Stock Exchange (BSE)

- Iceland:

- Iceland Stock Exchange (Kauphöll Íslands)

- Ireland:

- Italy:

- Latvia:

- Riga Stock Exchange (part of OMX)

- Lithuania:

- Vilnius Stock Exchange (part of OMX)

- Luxembourg:

- Macedonia:

- Malta:

- Montenegro

- Netherlands:

- Norway:

- Poland:

- Warsaw Stock Exchange (WSE)

- Portugal:

- Romania:

- Bucharest Stock Exchange (BSE)

- Sibiu Stock Exchange (SIBEX)

- Russia:

- Serbia:

- Belgrade Stock Exchange (BELEX)

- Slovakia:

- Bratislava Stock Exchange (BSSE)

- Slovenia:

- Ljubljana Stock Exchange (LJSE)

- Spain:

- Madrid Stock Exchange (IBEX 35)

- Sweden:

- Nordic Growth Market

- Stockholm Stock Exchange (part of OMX)

- Switzerland:

- Turkey:

- Istanbul Stock Exchange (ISE)

- Ukraine:

- United Kingdom:

- Alternative Investment Market (AIM)

- London Stock Exchange (LSE) (FTSE)

Economic sectors

Agriculture and fishing

Europe's agricultural sector is in general highly developed. The process of improving Central Europe's agriculture is ongoing and is helped by the accession of Central European states to the EU. The agricultural sector in Europe is helped by the Common Agricultural Policy (CAP), which provides farmers with a minimal price for their products and subsidizes their exports, which increases competitiveness for their products. This policy is highly controversial as it hampers free trade worldwide (protectionism sparks protectionism from other countries and trade blocs: the concept of trade wars) and is violating the concept of fair trade.

This means because of the protectionist nature of the CAP, agricultural products from developing countries are rendered incompetitive in both Europe (an important export market for developing countries) and on their home markets (as European agricultural products are dumped on developing countries' markets with help from European agricultural subsidies). This controversy surrounds every system of agricultural subsidies (the United States' policy of subsidizing farmers is also controversial). The CAP is also controversial because 40% of the EU's budget is spent on it, and because of the overproduction caused by it.

The Common Fisheries Policy is surrounded by an extensive system of rules (mainly consisting of quotas) to protect the environment from overfishing. Despite these rules, the cod is becoming increasingly rare in the North Sea resulting in drastic shortages in countries such as Canada and the United Kingdom. Strict fishing rules are the main reason for Norway and Iceland to stay out of the European Union (and out of the Common Fisheries Policy). Price guarantees and subsidizations of fishermen are implemented in the same way as agricultural subsidies are. Bluefin tuna is also a problem. Global stocks of the species are overfished with extinction in the wild a possibility in the near future. This also has the negative effect of threatening their traditional, natural predators.

Manufacturing

Europe has a thriving manufacturing sector, with a large part of the world's industrial production taking place in Europe. Most of the continent's industries are concentrated in the 'Blue Banana' (covering Southern England, the Benelux, western Germany, eastern France, Switzerland, and northern Italy). However, because of the higher wage level and hence production costs, Europe is suffering from deindustrialization and offshoring in the labour-intensive manufacturing sectors. This means that manufacturing has become less important and that jobs are moved to regions with cheaper labour costs (mainly China and Central and Eastern Europe).

Central Europe (Berlin, Saxony, the Czech Republic and Little Poland) was largely industrialised by 1850 [10] but Eastern Europe (European Russia) begun industrialisation between 1890–1900 and intensified it during the communist regime (as USSR) but it suffered from contraction in the 1990s when the inefficient heavy industry based manufacturing sector crippled after the collapse of communism and the introduction of the market economy.

In the 21st century the manufacturing sector in Central and Eastern Europe picked up because of the accession of ten formerly Communist European states to the EU and resulting accession to the European Common Market. This caused firms within the European Union to move jobs from their manufacturing sector to Central European countries such as Poland (see above), which sparked both Central and Eastern European industrial growth and employment.

According to Fortune Global 500, 195 of the top 500 companies are headquartered in Europe.[11] The main products in European industry are bicycles, rail, machinery, marine, aerospace equipment, food, chemical and pharmaceutical goods, software and electronics.

Investing and banking

Europe has a well-developed financial sector. Many European cities are financial centres with the City of London being the largest. The European financial sector is helped by the introduction of the euro as common currency. This has made it easier for European households and firms to invest in companies and deposit money on banks in other European countries. Exchange rate fluctuations are now non-existent in the Eurozone. The financial sector in Central and Eastern Europe is helped by economic growth in the region, European Regional Development Fund and the commitment of Central and Eastern European governments to achieve high standards.

European banks are amongst the largest and most profitable in the world (Barclays, BNP Paribas, Credit Agricole, Societe Generale, Royal Bank of Scotland, Deutsche Bank, UBS, National Trust, HSBC, Grupo Santander, BBVA, HBOS, Unicredit).[12]

Transport

Transport in Europe provides for the movement needs of over 700 million people[13] and associated freight. The political geography of Europe divides the continent into over 50 sovereign states and territories. This fragmentation, along with increased movement of people since the industrial revolution, has led to a high level of cooperation between European countries in developing and maintaining transport networks. Supranational and intergovernmental organisations such as the European Union (EU), Council of Europe and the Organization for Security and Co-operation in Europe have led to the development of international standards and agreements that allow people and freight to cross the borders of Europe, largely with unique levels of freedom and ease.

Rail transport

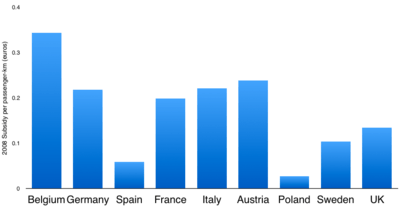

Rail networks in Western and Central Europe are often well maintained and well developed, whilst Eastern, Northern and Southern Europe often have less coverage and/or infrastructure problems. Electrified railway networks operate at a plethora of different voltages AC and DC varying from 750 to 25,000 volts, and signalling systems vary from country to country, hindering cross-border traffic. EU rail subsidies amounted to €73 billion in 2005.[15]

Air transport

Despite an extensive road and rail network, most long distance travel within Europe is by air. A large tourism industry also attracts many visitors to Europe, most of whom arrive into one of Europe's many large international airports. Frankfurt, London is the busiest airport in the world by number of international passengers (third busiest overall). The advent of low cost carriers in recent years has led to a large increase in air travel within Europe. Air transportation is now often the cheapest way of travelling between cities. This increase in air travel has led to problems of airspace overcrowding and environmental concerns. The Single European Sky is one initiative aimed at solving these problems.[16]

Global trade relations

The bulk of the EU's external trade is done with China, Mercosur and the United States,[17] Japan, Russia and non-member European states.

EU members are represented by a single official at the WTO.

The EU is involved in a few minor trade disputes. It had a long running dispute with the USA of allegedly unfair subsidies the US government gives to several companies, such as Boeing. The EU has a long running ban prohibiting arms trade with the Chinese. The EU issued a brief accusing Microsoft of predatory and monopolistic practices.

See also

Statistics:

- Organization for Security and Co-operation in Europe statistics

- International organisations in Europe

- List of European countries by budget revenues

- List of European countries by budget revenues per capita

- List of European countries by GDP (nominal)

- List of European countries by GDP (PPP)

- List of European countries by GDP (nominal) per capita

- List of European countries by GDP (PPP) per capita

- List of European countries by GNI (nominal) per capita

- List of European countries by GNI (PPP) per capita

- List of sovereign states in Europe by minimum wage

General:

Notes

| a. | ^ Kosovo is the subject of a territorial dispute between the Republic of Kosovo and the Republic of Serbia. The Republic of Kosovo unilaterally declared independence on 17 February 2008, but Serbia continues to claim it as part of its own sovereign territory. The two governments began to normalise relations in 2013, as part of the Brussels Agreement. Kosovo has received recognition as an independent state from 110 out of 193 United Nations member states. |

References

- ↑ . Last accessed 3 December 2010.

- ↑ "List of countries by GDP (Purchasing Power Parity) – CIA World Factbook". Cia.gov. Retrieved 26 April 2011.

- ↑ "List of countries by GDP (Official Exchange Rate) – CIA World Factbook". Cia.gov. Retrieved 26 April 2011.

- ↑ "Global Wealth Stages a Strong Comeback". Pr-inside.com. Retrieved 26 April 2011.

- ↑ "Global 500 2010: Countries – Australia". Fortune. Retrieved 8 July 2010. Number of companies data taken from the "Pick a country" box.

- ↑ "End of Millennium". google.co.uk.

- ↑ Responses to poverty: lessons from Europe by Robert Walker, Roger Lawson, and Peter Townsend

- ↑ GNI (nominal) per capita 2012, World Development Indicators database , World Bank, revised 12 Aug 2013, Atlas method

- ↑ "EUROPA – The euro". europa.eu.

- ↑ http://mbbnet.umn.edu/scmap/industrymap.html

- ↑ "PDF-Human Rights Policies and Management Practices: Results from questionnaire surveys of Governments and Fortune Global 500 firms" (PDF). Retrieved 6 March 2008.

- ↑ "Bank List – Top Banks in the World". Bankersalmanac.com. 16 February 2011. Retrieved 26 April 2011.

- ↑ "World Population Prospects: The 2008 Revision". United Nations Department of Economic and Social Affairs. 11 March 2009. Archived from the original on 12 October 2009. Retrieved 18 February 2010.

- ↑ "European rail study" (PDF). pp. 6, 44, 45.

2008 data is not provided for Italy, so 2007 data is used instead

- ↑ "EU Technical Report 2007".

- ↑ "The Single European Sky". European Organisation for the Safety of Air Navigation. 13 January 2009. Retrieved 18 February 2010.

- ↑ As regards the EU-China trade relations, see Paolo Farah (2006) Five Years of China's WTO Membership. EU and US Perspectives on China's Compliance with Transparency Commitments and the Transitional Review Mechanism, Legal Issues of Economic Integration, Kluwer Law International, Volume 33, Number 3, pp. 263–304.

External links

Media related to Economy of Europe at Wikimedia Commons

Media related to Economy of Europe at Wikimedia Commons